Life insurance is one of the most important financial tools available to protect your loved ones. Many people purchase life insurance because they want to ensure that their families remain financially secure even if something unexpected happens. However, one of the most common questions people ask is: How much life insurance coverage do you really need?

Buying too little coverage may leave your family struggling financially, while buying too much may cause unnecessary financial strain due to higher premiums. The right balance depends on your income, financial responsibilities, debts, lifestyle, and future goals.

This guide will explain everything you need to know about determining the right life insurance coverage for your situation. By understanding key factors and calculation methods, you can choose a policy that truly protects your family’s future.

Understanding the Purpose of Life Insurance

Before deciding how much coverage you need, it is important to understand the main purpose of life insurance.

Life insurance provides financial support to your dependents after your death. The payout from a life insurance policy, also known as the death benefit, can help cover various financial responsibilities such as:

-

Daily living expenses

-

Mortgage or rent payments

-

Children’s education costs

-

Outstanding debts

-

Funeral and burial expenses

-

Long-term financial goals

For many families, the sudden loss of income can be devastating. Life insurance acts as a financial safety net that helps maintain stability during a difficult time.

Why Choosing the Right Coverage Amount Matters

Selecting the right coverage amount is critical for financial protection. If your coverage is too low, your family might struggle to maintain their lifestyle or meet important financial obligations.

On the other hand, extremely high coverage may lead to expensive premiums that could strain your monthly budget.

The goal is to find a coverage amount that:

-

Replaces lost income

-

Pays off debts

-

Covers future financial goals

-

Provides stability for your dependents

When chosen carefully, life insurance becomes a powerful tool for long-term financial planning.

Key Factors That Determine Life Insurance Needs

Several important factors influence how much life insurance coverage you should purchase.

1. Your Current Income

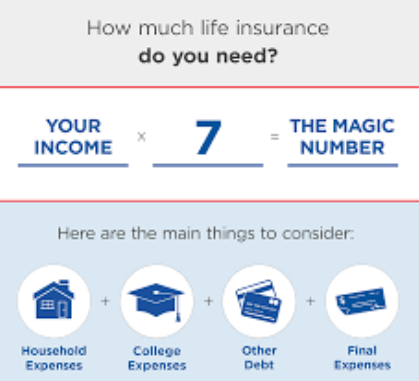

Your income is one of the most significant factors in determining coverage. If your family depends on your salary to cover everyday expenses, the insurance payout should replace that income for several years.

Financial experts often recommend coverage equal to 10 to 15 times your annual income, but this is only a general guideline. Your personal financial situation may require more or less coverage.

2. Number of Dependents

Dependents include anyone who relies on your income, such as:

-

Spouse

-

Children

-

Elderly parents

-

Disabled family members

The more dependents you have, the higher your life insurance coverage should be.

For example, a single person with no dependents may need minimal coverage, while a parent with three children may require a much larger policy.

3. Outstanding Debts

Another critical factor is your existing debt obligations. Life insurance can ensure that your family does not inherit financial burdens.

Common debts include:

-

Mortgage loans

-

Car loans

-

Personal loans

-

Credit card debt

-

Student loans

When calculating life insurance coverage, include the total amount needed to pay off these debts.

Considering Your Family’s Future Expenses

Life insurance should also account for future financial needs, not just current obligations.

Children’s Education

Education costs continue to rise around the world. If you have children, life insurance can help ensure they can still attend college or university even if you are no longer there to support them.

Consider the cost of:

-

Tuition fees

-

Books and supplies

-

Housing

-

Other academic expenses

Planning for these costs in advance ensures that your children’s education will not be disrupted.

Daily Living Expenses

Your family will still need money for everyday expenses such as:

-

Food

-

Utilities

-

Transportation

-

Healthcare

-

Clothing

A well-planned life insurance policy should cover several years of living expenses.

Accounting for Funeral and Final Expenses

Funeral and burial costs can be surprisingly expensive. In many countries, funeral services can cost thousands of dollars.

Typical final expenses include:

-

Funeral service

-

Burial or cremation

-

Medical bills

-

Legal and administrative costs

Although these expenses may seem small compared to other financial obligations, including them in your life insurance coverage ensures your family does not face additional financial stress during an already difficult time.

Popular Methods to Calculate Life Insurance Needs

There are several common methods used to estimate the right life insurance coverage amount.

1. The Income Replacement Method

The income replacement method focuses on replacing your income for a certain number of years.

For example:

If you earn $50,000 per year and want to replace your income for 15 years:

$50,000 × 15 = $750,000 coverage

This method provides a simple estimate but may not account for all financial responsibilities.

2. The DIME Method

The DIME method is one of the most widely used strategies for calculating life insurance coverage. DIME stands for:

D – Debt

Total outstanding debts excluding mortgage.

I – Income

Amount of income your family will need to replace for several years.

M – Mortgage

Remaining mortgage balance.

E – Education

Future education costs for children.

By adding these four categories together, you can estimate your ideal life insurance coverage.

Example:

-

Debt: $20,000

-

Income replacement: $500,000

-

Mortgage: $200,000

-

Education: $100,000

Total coverage needed: $820,000

3. The Human Life Value Approach

The Human Life Value method estimates the total economic value of your life based on your future earnings.

This method considers:

-

Current income

-

Future salary growth

-

Years until retirement

-

Taxes

-

Living expenses

Although more complex, it provides a detailed estimate of the financial value you contribute to your family.

How Age Affects Life Insurance Coverage

Age plays a major role in determining both the cost and the amount of life insurance coverage you need.

Younger Individuals

Younger individuals often require larger coverage because they have many years of financial responsibility ahead of them.

They may need to cover:

-

Long-term income replacement

-

Mortgage payments

-

Childcare and education costs

However, premiums are usually lower for younger policyholders, making it a good time to purchase life insurance.

Older Individuals

As people grow older, financial responsibilities may decrease.

For example:

-

Children may become financially independent

-

Mortgage loans may be paid off

-

Retirement savings may increase

In such cases, life insurance needs may decrease over time.

Stay-at-Home Parents and Life Insurance

Many people assume that stay-at-home parents do not need life insurance because they do not earn an income. However, their contribution to the household has significant economic value.

Stay-at-home parents often provide services such as:

-

Childcare

-

Cooking

-

Cleaning

-

Transportation

-

Household management

If these responsibilities had to be outsourced, the costs could be very high. Life insurance for stay-at-home parents can help cover these expenses if something unexpected happens.

Single Individuals and Life Insurance Needs

Single individuals without dependents may not need large life insurance policies. However, they may still benefit from some coverage.

Reasons include:

-

Covering funeral expenses

-

Paying off personal debts

-

Leaving financial support for parents or siblings

A smaller policy can provide peace of mind without large monthly premiums.

Business Owners and Life Insurance

For business owners, life insurance can play an important role in business continuity.

It can help:

-

Protect business partners

-

Cover business debts

-

Fund buy-sell agreements

-

Maintain operations during leadership transitions

Without proper coverage, a business may struggle financially after the loss of a key owner.

Inflation and Its Impact on Life Insurance Coverage

Inflation gradually reduces the purchasing power of money. A life insurance policy purchased today may be worth less in the future if inflation is not considered.

For example, a policy worth $500,000 today may not provide the same financial security 20 years later.

To address this issue, some policies offer:

-

Inflation protection riders

-

Increasing coverage options

-

Periodic policy reviews

These features help ensure your life insurance coverage keeps up with rising living costs.

Reviewing Your Life Insurance Coverage Regularly

Life insurance needs are not static. As your life changes, your coverage should be reviewed and updated.

Major life events that may require policy adjustments include:

-

Marriage

-

Birth of a child

-

Buying a home

-

Career changes

-

Divorce

-

Retirement

Reviewing your policy every few years ensures that your coverage remains aligned with your financial responsibilities.

Common Mistakes When Choosing Coverage

Many people make mistakes when selecting life insurance coverage. Avoiding these common errors can help you make better financial decisions.

Underestimating Financial Needs

Some individuals choose the minimum coverage to save money on premiums. Unfortunately, this may leave their family financially vulnerable.

Ignoring Future Expenses

Focusing only on current expenses may lead to inadequate coverage. Future needs like education or healthcare should also be considered.

Not Updating Coverage

Life changes quickly, and failing to update your policy can lead to outdated coverage that no longer meets your family’s needs.

Term Life vs Whole Life Coverage Considerations

The type of life insurance you choose may also affect how much coverage you need.

Term Life Insurance

Term life insurance provides coverage for a specific period, such as:

-

10 years

-

20 years

-

30 years

It usually offers higher coverage at lower premiums, making it popular for income replacement.

Whole Life Insurance

Whole life insurance provides lifelong coverage and may include a savings or investment component.

Although premiums are higher, it can offer additional financial benefits such as cash value accumulation.

Choosing the right policy type depends on your long-term financial goals.

How to Balance Coverage and Affordability

Finding the right balance between adequate coverage and affordable premiums is essential.

Consider these strategies:

-

Compare policies from multiple insurers

-

Start coverage early when premiums are lower

-

Choose a term length that matches your financial responsibilities

-

Avoid unnecessary add-ons unless they provide real value

The goal is to secure strong protection without putting pressure on your monthly budget.

Using Online Life Insurance Calculators

Many insurance providers offer online life insurance calculators that help estimate coverage needs.

These tools typically ask for information such as:

-

Age

-

Income

-

Debts

-

Savings

-

Number of dependents

-

Financial goals

While these calculators can provide helpful estimates, they should be used as a starting point rather than a final decision.

When to Seek Professional Financial Advice

Life insurance planning can sometimes be complex, especially for individuals with large families, significant debts, or business interests.

A financial advisor can help:

-

Evaluate your financial situation

-

Calculate accurate coverage needs

-

Compare policy options

-

Develop long-term financial strategies

Professional guidance can help ensure that your life insurance plan aligns with your overall financial goals.

Final Thoughts

Determining how much life insurance coverage you need is a crucial step in protecting your family’s financial future. The right coverage amount depends on several factors, including income, debts, dependents, and long-term financial goals.

By considering income replacement, future expenses, debt obligations, and lifestyle needs, you can choose a policy that truly supports your loved ones in difficult times.