Life insurance plays an important role in financial planning. It protects your family financially if something happens to you and ensures your loved ones are not left struggling with debts, living expenses, or major financial obligations. When exploring life insurance options, two of the most common types you will encounter are term life insurance and whole life insurance.

Although both provide a death benefit to beneficiaries, they differ greatly in terms of coverage duration, cost, flexibility, and investment features. Understanding the difference between these two policies is essential before deciding which one is right for you.

This comprehensive guide explains how term life and whole life insurance work, their advantages and disadvantages, and how to choose the best option for your financial goals.

Understanding Life Insurance Basics

Before diving into the comparison, it is important to understand what life insurance is and how it works.

Life insurance is a contract between an individual and an insurance company. The policyholder pays regular premiums, and in return the insurer promises to pay a death benefit to designated beneficiaries if the insured person dies while the policy is active.

This payout can help cover expenses such as:

-

Funeral costs

-

Mortgage payments

-

Education expenses

-

Outstanding debts

-

Daily living expenses

Most policies provide tax-free death benefits to beneficiaries, making life insurance a powerful financial protection tool.

However, the type of policy you choose determines how long coverage lasts, how much you pay, and whether the policy builds any financial value over time.

What Is Term Life Insurance?

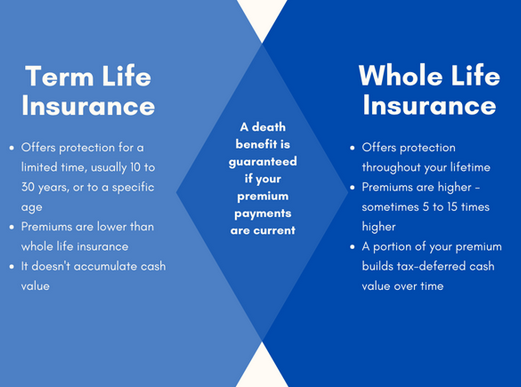

Term life insurance is the simplest and most affordable type of life insurance. It provides coverage for a specific period of time, known as the term.

Common term lengths include:

-

10 years

-

20 years

-

30 years

If the insured person dies during the policy term, the beneficiaries receive the death benefit. However, if the policyholder outlives the term, the coverage expires and no payout is made.

Because term life insurance is temporary and does not include investment components, premiums are usually much lower than permanent life insurance policies.

Key Features of Term Life Insurance

1. Fixed Coverage Period

Term policies last only for a specified time. Once the term ends, coverage expires unless renewed.

2. Lower Premiums

Term life insurance is significantly cheaper than whole life insurance because it provides temporary protection.

3. Simple Structure

Term life policies are easy to understand. You pay premiums for coverage, and if death occurs during the term, your family receives the benefit.

4. No Cash Value

Unlike permanent policies, term life does not accumulate savings or investment value.

5. Renewable or Convertible Options

Some policies allow conversion to permanent insurance or renewal after the term ends, though renewal premiums may increase significantly.

What Is Whole Life Insurance?

Whole life insurance is a type of permanent life insurance that lasts for the insured person’s entire lifetime as long as premiums are paid.

Unlike term life insurance, whole life policies also include a cash value component, which grows over time. This savings feature can be borrowed against or withdrawn during the policyholder’s lifetime.

Whole life insurance combines life insurance protection with a financial asset that grows steadily over time.

Key Features of Whole Life Insurance

1. Lifetime Coverage

Whole life policies provide coverage for life instead of a limited term.

2. Cash Value Accumulation

Part of the premium goes toward a cash value account that grows at a guaranteed rate.

3. Fixed Premiums

Premium payments remain consistent throughout the life of the policy.

4. Ability to Borrow Against the Policy

Policyholders can take loans against the cash value for emergencies, investments, or other financial needs.

5. Potential Dividends

Some policies may pay dividends depending on the insurer’s performance.

Because of these features, whole life insurance premiums are significantly higher than term life premiums.

Key Differences Between Term Life and Whole Life Insurance

Understanding the core differences between these policies can help determine which one best fits your financial goals.

1. Coverage Duration

Term life insurance offers protection for a limited period, usually between 10 and 30 years. Once the policy expires, coverage ends unless renewed.

Whole life insurance provides lifelong coverage, ensuring beneficiaries receive the death benefit whenever the policyholder passes away.

2. Cost of Premiums

One of the biggest differences between the two policies is cost.

Term life insurance is significantly cheaper because it provides temporary protection. Whole life insurance can cost five to fifteen times more than a comparable term policy due to its permanent coverage and cash value component.

The higher premiums of whole life insurance fund both the insurance coverage and the cash value account.

3. Cash Value Component

Term life insurance does not build cash value. If the policyholder outlives the policy term, there is no financial return.

Whole life insurance builds cash value that grows over time and can be accessed through loans or withdrawals.

This feature makes whole life insurance a combination of insurance and long-term savings.

4. Investment and Savings Element

Whole life insurance can serve as a conservative savings vehicle because the cash value grows on a tax-deferred basis.

Term life insurance, however, focuses solely on providing financial protection for beneficiaries.

Many financial advisors recommend buying term insurance and investing the difference in other assets like retirement accounts or mutual funds.

5. Flexibility

Term life insurance offers flexibility because you can choose different coverage lengths depending on your needs.

Whole life insurance requires a long-term financial commitment due to its higher premiums and lifetime coverage.

Pros and Cons of Term Life Insurance

Advantages

Affordable Coverage

Term policies are much cheaper than permanent life insurance, making them accessible to most families.

Higher Coverage for Less Money

Because premiums are lower, individuals can afford higher coverage amounts.

Ideal for Temporary Needs

Term life works well for covering specific financial responsibilities like raising children or paying off a mortgage.

Simplicity

These policies are straightforward and easy to understand.

Disadvantages

Coverage Expires

If the policyholder survives the term, coverage ends with no payout.

No Cash Value

Term life insurance does not accumulate savings.

Higher Renewal Costs

Renewing coverage after the term may be significantly more expensive due to age and health changes.

Pros and Cons of Whole Life Insurance

Advantages

Lifetime Coverage

Whole life insurance ensures beneficiaries receive a payout regardless of when the policyholder dies.

Cash Value Growth

The policy builds cash value that can serve as an emergency fund or supplemental retirement income.

Stable Premiums

Premiums remain fixed throughout the life of the policy.

Financial Planning Tool

Whole life insurance can play a role in estate planning and long-term wealth strategies.

Disadvantages

High Premiums

Whole life insurance costs significantly more than term life insurance.

Lower Investment Returns

Cash value growth is generally slower than returns from stocks or other investments.

Complex Structure

Whole life policies can be more difficult to understand due to their financial components.

When Term Life Insurance Makes More Sense

Term life insurance is typically the best option for individuals who need affordable coverage for a specific period.

Ideal situations include:

Young families

Parents with young children often need protection until their children become financially independent.

Mortgage protection

Term insurance can ensure the mortgage is paid if the primary earner dies.

Income replacement

It protects your family’s financial stability during your working years.

Budget constraints

Term insurance allows people to obtain large coverage amounts at low cost.

Because of these benefits, term life insurance is often recommended for most families.

When Whole Life Insurance May Be Better

Whole life insurance may be suitable for individuals with long-term financial planning needs.

It may be beneficial if:

You want lifelong coverage

Whole life ensures your beneficiaries will receive a payout regardless of when you pass away.

You need estate planning tools

High-net-worth individuals often use permanent insurance to transfer wealth to heirs.

You want forced savings

The cash value component encourages long-term saving.

You want tax-advantaged financial growth

Cash value growth is tax-deferred and loans can often be taken tax-free.

However, these benefits are typically most valuable for individuals with higher incomes or complex financial plans.

Cost Comparison: Term vs Whole Life

To better understand the difference, consider a hypothetical example:

30-year-old healthy individual

| Policy Type | Coverage | Monthly Premium |

|---|---|---|

| Term Life (20-year) | $500,000 | $20–$40 |

| Whole Life | $500,000 | $300–$500 |

While exact prices vary by insurer, the difference shows why term insurance is more accessible for most people.

Can You Combine Term and Whole Life Insurance?

Yes. Some people choose to combine both policies as part of their financial strategy.

For example:

-

Buy a large term policy to protect income during working years

-

Maintain a smaller whole life policy for lifelong coverage and estate planning

This approach provides affordable protection while still benefiting from permanent insurance features.

Important Factors to Consider Before Choosing

Choosing between term and whole life insurance requires careful evaluation of your financial situation.

Budget

If affordability is your main concern, term life insurance is usually the better option.

Financial Goals

Consider whether you want pure protection or a policy that includes a savings component.

Family Responsibilities

People with dependents often prioritize large, affordable coverage.

Long-Term Planning

Whole life insurance may make sense for estate planning or wealth transfer strategies.

Age and Health

The younger and healthier you are, the cheaper your premiums will be.

Insurance companies also evaluate factors such as health conditions, lifestyle habits, and family medical history when determining premiums.

Common Myths About Life Insurance

Myth 1: Whole Life Insurance Is Always Better

Whole life insurance offers unique benefits, but it is not necessarily the best choice for everyone.

For many families, term insurance provides more coverage at a fraction of the cost.

Myth 2: Term Insurance Is a Waste of Money

Some people believe term insurance is wasted if they outlive the policy.

However, the purpose of insurance is protection—not investment. Term insurance protects families during their most financially vulnerable years.

Myth 3: You Only Need Life Insurance When You Are Older

Life insurance is often cheaper when purchased at a younger age. Buying early can lock in lower premiums.

How to Decide Which Policy Is Right for You

Choosing between term and whole life insurance ultimately depends on your personal financial situation.

A simple rule many experts suggest is:

Buy term insurance for protection and invest separately for growth.

However, if you want permanent coverage and a guaranteed savings component, whole life insurance may suit your needs.

Final Verdict: Term Life vs Whole Life Insurance

Both term life insurance and whole life insurance serve valuable purposes, but they are designed for different financial goals.

Term life insurance is best for:

-

Affordable coverage

-

Young families

-

Income replacement

-

Temporary financial protection

Whole life insurance is best for:

-

Lifelong coverage

-

Estate planning

-

Wealth transfer strategies

-

Individuals who want a built-in savings component

For most people, especially young families and individuals with limited budgets, term life insurance is the most practical and cost-effective choice.

However, those seeking permanent coverage and long-term financial planning tools may benefit from whole life insurance.