Car insurance is one of the most important financial protections a driver can have. Whether you drive a brand-new car or an older vehicle, insurance helps protect you from potentially devastating financial losses caused by accidents, theft, or natural disasters. Among the different types of auto insurance available, full coverage car insurance is often considered the most comprehensive option.

However, many drivers wonder whether full coverage insurance is really worth the extra cost. While it offers broader protection compared to minimum liability insurance, it also comes with higher premiums and other considerations. Understanding the advantages and disadvantages of full coverage insurance can help you decide whether it’s the right choice for your situation.

This guide explores what full coverage car insurance is, what it includes, its major benefits and drawbacks, and when it makes financial sense to buy it.

What Is Full Coverage Car Insurance?

The term “full coverage car insurance” does not refer to a specific policy sold by insurance companies. Instead, it typically describes a combination of multiple types of coverage designed to provide broader protection for drivers.

Most full coverage policies include three primary components:

Liability Insurance

Liability insurance covers damages or injuries you cause to other people in an accident. It usually includes:

-

Bodily injury liability: Pays for medical expenses, lost wages, and legal costs if someone is injured because of an accident you caused.

-

Property damage liability: Pays for damage to another person’s property, such as their car, building, or fence.

Liability coverage is usually required by law in most places and forms the basic foundation of any auto insurance policy.

Collision Coverage

Collision insurance pays for damage to your own vehicle if you collide with another vehicle or object, regardless of who is at fault. This includes accidents such as:

-

Crashing into another car

-

Hitting a pole or guardrail

-

Rolling your vehicle

Comprehensive Coverage

Comprehensive coverage protects your car against non-collision events such as:

-

Theft

-

Fire

-

Vandalism

-

Floods or storms

-

Falling objects

-

Animal collisions

Together, these three types of coverage provide much broader financial protection than liability insurance alone.

What Full Coverage Car Insurance Typically Covers

A full coverage policy helps pay for a wide range of situations that can damage your vehicle or cause financial losses.

Accidents You Cause

If you cause an accident, liability coverage pays for injuries or property damage suffered by others.

Damage to Your Own Vehicle

Collision coverage pays for repairs or replacement of your own car after an accident.

Theft or Vandalism

Comprehensive coverage pays if your vehicle is stolen or vandalized.

Natural Disasters

Events like hailstorms, floods, earthquakes, and fires are usually covered.

Animal Collisions

If you hit a deer or another animal, comprehensive coverage can help pay for the damage.

Legal Costs

If someone sues you after an accident, liability insurance often covers legal defense costs.

What Full Coverage Insurance Does NOT Cover

Despite the name, full coverage does not cover everything. Drivers sometimes misunderstand the term and assume it includes every possible risk.

Common exclusions include:

-

Mechanical breakdowns

-

Regular wear and tear

-

Damage from illegal activities

-

Racing or off-road use

-

Business use of a personal vehicle

-

Personal belongings inside the car

Additional coverage such as roadside assistance, rental reimbursement, or gap insurance may need to be purchased separately.

Pros of Full Coverage Car Insurance

Full coverage insurance provides several important benefits, especially for drivers who want strong financial protection.

1. Greater Financial Protection

One of the biggest advantages of full coverage insurance is the financial protection it offers.

Without full coverage, you would have to pay out-of-pocket for repairs or replacement of your vehicle after an accident. With full coverage, the insurer covers these costs up to the policy limits.

Car repairs can easily cost thousands of dollars, so this protection can be extremely valuable.

2. Protection Against Theft and Natural Disasters

Vehicles can be damaged or destroyed even when they are not involved in accidents. For example:

-

A severe storm could damage your car

-

A tree could fall on it

-

Someone could vandalize or steal it

Comprehensive coverage protects against these risks.

3. Coverage Even When You Are at Fault

With liability-only insurance, your policy pays for damage to other people’s vehicles but not your own car.

Full coverage includes collision insurance, which means your car can be repaired even if you caused the accident.

4. Required for Financed or Leased Cars

If your car is financed or leased, lenders usually require full coverage insurance to protect their investment.

Without it, you may violate the terms of your loan agreement.

5. Peace of Mind

Many drivers choose full coverage simply because it offers peace of mind.

Knowing that your car is protected from accidents, theft, and disasters can reduce stress and financial uncertainty.

6. Additional Optional Benefits

Many insurers allow drivers to add extra protections such as:

-

Roadside assistance

-

Rental car reimbursement

-

Gap insurance

-

Uninsured motorist coverage

These additional features can make your policy even more comprehensive.

Cons of Full Coverage Car Insurance

While full coverage provides strong protection, it also comes with several drawbacks that drivers should consider.

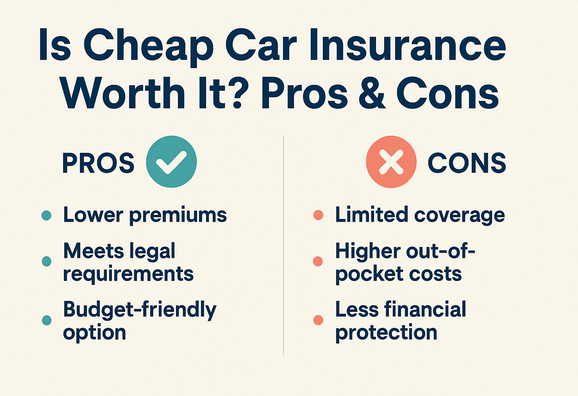

1. Higher Insurance Premiums

The biggest disadvantage of full coverage insurance is the cost.

Adding collision and comprehensive coverage significantly increases the price of your policy. Full coverage insurance costs considerably more than liability-only coverage because it protects both your vehicle and others involved in an accident.

For drivers on a tight budget, these higher premiums may not be affordable.

2. Deductibles Apply

When you file a claim under collision or comprehensive coverage, you usually must pay a deductible.

For example, if you have a $500 deductible and $2,000 in damage, your insurance company will pay $1,500 while you pay $500.

Higher deductibles can reduce your premium, but they increase out-of-pocket costs during claims.

3. Not Always Cost-Effective for Older Cars

If your car is older and has a low market value, full coverage may not be worth the price.

For example:

-

Your car may be worth $3,000

-

You pay $1,200 per year for full coverage

In this situation, the premiums may exceed the value of the car over time.

4. Depreciation Reduces Payouts

Insurance companies typically pay the actual cash value of your car at the time of the claim.

Since cars lose value over time, the payout may be lower than expected.

5. Policy Limits and Exclusions

Full coverage policies still have limits and exclusions.

If damages exceed the policy limits, you may still need to pay additional costs.

6. Premiums May Increase After Claims

Filing insurance claims can sometimes increase your future premiums.

Drivers who make frequent claims may see significant increases in insurance costs.

Full Coverage vs Liability-Only Insurance

Understanding the difference between full coverage and liability-only insurance can help drivers make better decisions.

Liability-Only Insurance

Liability insurance covers:

-

Damage to other people’s vehicles

-

Injuries caused to other drivers

-

Legal expenses

However, it does not cover your own vehicle.

Full Coverage Insurance

Full coverage includes liability plus:

-

Collision coverage

-

Comprehensive coverage

This means your car is also protected from accidents and other damages.

Because of this broader protection, full coverage insurance costs significantly more than liability-only policies.

When Full Coverage Car Insurance Is Worth It

Full coverage insurance can be a smart investment in several situations.

1. Your Car Is New or Expensive

If your car has a high market value, replacing it out of pocket would be expensive.

Full coverage protects that investment.

2. You Have a Car Loan or Lease

Most lenders require full coverage until the loan is fully paid off.

This ensures the vehicle remains protected even if it is damaged or destroyed.

3. You Cannot Afford Major Repairs

If paying thousands of dollars for repairs would create financial hardship, full coverage may be worth the cost.

4. You Live in a High-Risk Area

Drivers living in areas with high rates of:

-

Vehicle theft

-

Severe weather

-

Traffic accidents

may benefit from full coverage protection.

When Full Coverage May Not Be Worth It

In some situations, paying for full coverage may not make financial sense.

1. Your Car Has Low Market Value

If your car is worth only a few thousand dollars, the cost of full coverage may exceed the potential payout.

Many financial experts recommend dropping collision and comprehensive coverage once a car’s value becomes very low.

2. You Can Easily Replace the Car

If you have enough savings to replace your car without financial strain, you may not need full coverage.

3. Insurance Premiums Are Too High

Young drivers or those with poor driving records often face very high premiums.

In such cases, liability insurance may be a more affordable option.

4. The 10% Rule

Some financial experts suggest a simple rule:

If the annual premium for full coverage exceeds 10% of the car’s value, it may be time to reconsider the policy.

Factors That Affect Full Coverage Insurance Cost

Insurance companies calculate premiums using several factors, including:

Driving Record

Drivers with accidents or traffic violations usually pay higher premiums.

Age and Experience

Young drivers typically pay more because they are considered higher risk.

Vehicle Type

Expensive or high-performance cars usually cost more to insure.

Location

Insurance costs vary depending on accident rates, theft rates, and weather risks.

Deductible Amount

Higher deductibles generally lower premiums.

Tips for Saving Money on Full Coverage Insurance

Drivers can still enjoy the benefits of full coverage while keeping costs manageable.

Compare Multiple Insurance Quotes

Different insurers offer different prices, so shopping around can save money.

Increase Your Deductible

A higher deductible reduces your monthly premium.

Bundle Insurance Policies

Many insurers offer discounts if you combine auto and home insurance.

Maintain a Good Driving Record

Safe drivers often receive lower premiums.

Ask About Discounts

Insurers may offer discounts for:

-

Safe driving

-

Low mileage

-

Good student records

-

Anti-theft devices

Common Myths About Full Coverage Insurance

Many drivers misunderstand how full coverage works.

Myth 1: Full Coverage Means Everything Is Covered

In reality, policies still have exclusions and limits.

Myth 2: Full Coverage Is Required by Law

Most places only require liability insurance.

Myth 3: Older Cars Always Need Full Coverage

For older vehicles, full coverage may not be financially worthwhile.

Final Verdict: Is Full Coverage Car Insurance Worth It?

Full coverage car insurance can be a valuable financial safeguard, especially for drivers with newer vehicles or those who want strong protection against unexpected losses.

It offers broader protection than liability-only insurance by covering damage to your own vehicle as well as others involved in an accident. However, this protection comes with higher premiums and deductibles.

Ultimately, whether full coverage insurance is worth it depends on factors such as:

-

The value of your vehicle

-

Your financial situation

-

Your tolerance for risk

-

The cost of insurance premiums

For many drivers, full coverage provides essential peace of mind and financial security. For others with older vehicles or tight budgets, liability-only insurance may be the more practical choice.