Car insurance is one of the most important financial protections a vehicle owner can have. Whether you drive daily to work, travel frequently, or simply use your car occasionally, having the right insurance coverage protects you from potentially large financial losses. One key concept that many drivers struggle to fully understand is the car insurance deductible.

When choosing a car insurance policy, you will almost always be asked to select a deductible amount. This number directly affects how much you pay for your insurance premium and how much you pay out of pocket if you file a claim. Because of this, selecting the right deductible is an important financial decision.

In this detailed guide, we will explain what car insurance deductibles are, how they work, the different types of deductibles, the relationship between deductibles and premiums, and how to decide the best deductible amount for your situation.

What Is a Car Insurance Deductible?

A car insurance deductible is the amount of money you must pay out of pocket before your insurance company pays the rest of a covered claim.

In simple terms, it is the portion of repair or replacement costs that you are responsible for paying yourself.

For example:

-

Your deductible: $500

-

Repair cost after an accident: $3,000

You pay the first $500, and the insurance company covers the remaining $2,500.

Deductibles apply mainly to certain types of coverage such as:

-

Collision coverage

-

Comprehensive coverage

-

Personal injury protection (in some policies)

However, deductibles usually do not apply to liability coverage, which pays for damage or injuries you cause to others.

Why Do Insurance Policies Have Deductibles?

Insurance companies use deductibles for several important reasons.

1. Reducing Small Claims

Without deductibles, drivers might file claims for minor damages such as small scratches or dents. Deductibles discourage unnecessary claims.

2. Lowering Insurance Fraud

When drivers must share part of the cost, the likelihood of fraudulent claims decreases.

3. Sharing Risk Between Driver and Insurer

Deductibles ensure that both the insurance company and the driver share responsibility for losses.

4. Controlling Premium Costs

Higher deductibles allow insurers to offer lower monthly premiums.

Types of Car Insurance Deductibles

Not all deductibles work exactly the same way. Understanding the different types helps you choose the best option.

Collision Deductible

Collision coverage helps pay for damage to your vehicle when it collides with:

-

Another vehicle

-

A tree or pole

-

A building

-

A guardrail

Example:

If you crash into another car and the repair cost is $4,000 with a $1,000 deductible, you pay $1,000 and the insurer pays $3,000.

Comprehensive Deductible

Comprehensive coverage protects your car from non-collision incidents, such as:

-

Theft

-

Vandalism

-

Fire

-

Natural disasters

-

Falling objects

-

Animal collisions

Example:

If a tree branch falls on your car causing $2,500 in damage and your deductible is $500, you pay $500 while the insurance company pays $2,000.

Glass Deductible

Some policies include a separate deductible for windshield or glass damage. In certain cases, insurers even waive the deductible for windshield repairs.

This means small cracks might be repaired without any out-of-pocket cost.

Disappearing Deductible

Some insurance companies offer a vanishing deductible program. If you maintain safe driving habits and avoid accidents for several years, your deductible gradually decreases.

For example:

-

Starting deductible: $500

-

After one claim-free year: $450

-

After two years: $400

This reward encourages safe driving.

Common Car Insurance Deductible Amounts

Insurance companies typically offer several deductible options. The most common choices include:

-

$250

-

$500

-

$750

-

$1,000

-

$1,500

-

$2,000

Most drivers choose $500 or $1,000, as these offer a balanced combination of affordable premiums and manageable out-of-pocket costs.

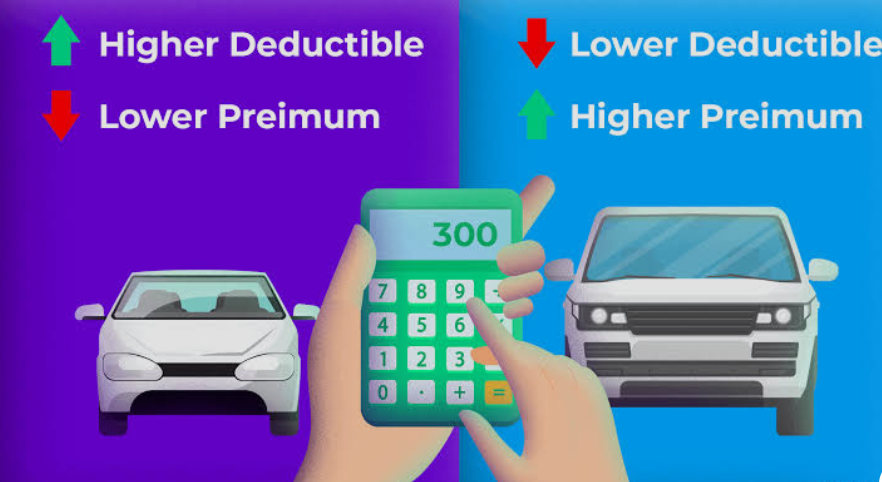

How Deductibles Affect Insurance Premiums

Your deductible amount has a direct impact on how much you pay for car insurance.

Higher Deductible = Lower Premium

When you choose a higher deductible, you take on more financial risk. Because of this, the insurance company charges you lower monthly premiums.

Example:

-

$250 deductible → higher premium

-

$1,000 deductible → lower premium

Lower Deductible = Higher Premium

If you select a lower deductible, the insurance company will have to pay more during claims. As a result, they charge higher premiums.

Example:

-

$250 deductible → insurance pays more → higher cost for you

Example: Deductible vs Premium Comparison

Let’s look at a simple example.

| Deductible | Monthly Premium | Annual Premium |

|---|---|---|

| $250 | $150 | $1,800 |

| $500 | $130 | $1,560 |

| $1,000 | $110 | $1,320 |

In this example, choosing a $1,000 deductible instead of $250 saves $480 per year.

However, if you have an accident, you must pay more out of pocket.

When Do You Pay a Deductible?

You only pay a deductible when filing a claim for covered damage.

Situations where you may need to pay a deductible include:

-

Car accidents

-

Theft

-

Storm damage

-

Vandalism

-

Animal collisions

However, you may not need to pay a deductible if another driver is clearly at fault and their insurance covers the damage.

Situations Where Deductibles May Not Apply

There are several cases where you might not have to pay a deductible.

If Another Driver Is at Fault

If another driver caused the accident and their insurance company accepts liability, their insurance should pay the damages.

Windshield Repair Programs

Many insurers waive deductibles for small windshield repairs.

Liability Claims

Liability coverage pays for damage to other people’s property or injuries you cause. Deductibles usually do not apply.

How to Choose the Right Deductible

Choosing the right deductible depends on several personal financial factors.

1. Your Emergency Savings

The most important question to ask is:

Could you comfortably pay the deductible if an accident happened tomorrow?

If you cannot afford a $1,000 repair payment, choosing a high deductible could create financial stress.

2. Your Driving Habits

Drivers who spend a lot of time on the road face higher accident risks.

Factors include:

-

Daily commuting

-

Driving in heavy traffic

-

Long-distance travel

Frequent drivers may prefer a lower deductible for extra protection.

3. Your Vehicle’s Value

The value of your car should influence your deductible decision.

For older vehicles with lower market value, a very low deductible may not make financial sense.

Example:

If your car is worth $3,000, paying high premiums for a $250 deductible might not be worthwhile.

4. Your Risk Tolerance

Some drivers prefer lower premiums even if it means higher risk.

Others prefer financial security and predictable costs.

Your comfort level with financial risk should guide your choice.

High Deductible vs Low Deductible

Let’s compare both options.

High Deductible Advantages

-

Lower monthly premiums

-

Long-term savings on insurance costs

-

Encourages careful driving

High Deductible Disadvantages

-

Higher out-of-pocket cost after accidents

-

May be difficult during financial emergencies

Low Deductible Advantages

-

Smaller out-of-pocket expense during claims

-

Less financial stress after accidents

Low Deductible Disadvantages

-

Higher insurance premiums

-

Higher total insurance costs over time

When a High Deductible Makes Sense

A higher deductible can be a smart choice in several situations:

-

You have strong emergency savings

-

You rarely drive

-

You have a safe driving record

-

You want lower monthly premiums

Many financially stable drivers choose deductibles between $1,000 and $2,000 to reduce insurance costs.

When a Low Deductible Is Better

A lower deductible might be better if:

-

You have limited savings

-

You drive frequently

-

You live in a high-accident area

-

You prefer predictable costs

Drivers with tight budgets often feel more comfortable with $250 or $500 deductibles.

Deductibles and Leasing or Financing

If your car is leased or financed, lenders often require certain insurance coverage levels.

They may also limit the deductible you can choose.

For example:

A lender might require:

-

Maximum deductible: $1,000

This protects the lender’s financial interest in the vehicle.

How Deductibles Work for Multiple Claims

Each claim usually requires a separate deductible payment.

Example:

Accident repair: $3,000 → $500 deductible

Storm damage months later: $2,000 → another $500 deductible

You would pay $1,000 total across two claims.

Tips for Managing Your Deductible

Here are some practical strategies to handle deductible costs.

Create an Emergency Fund

Setting aside money for unexpected car repairs helps you comfortably afford higher deductibles.

Balance Premium Savings

Calculate how much you save annually with a higher deductible.

If the savings exceed the deductible difference over time, it might be worth choosing the higher option.

Review Your Policy Annually

As your financial situation improves, you may want to adjust your deductible to reduce insurance costs.

Common Mistakes When Choosing a Deductible

Many drivers make avoidable mistakes when selecting their deductible.

Choosing the Cheapest Premium

Low premiums can be attractive, but extremely high deductibles may create financial problems during accidents.

Ignoring Savings Potential

Some drivers keep very low deductibles for years without realizing how much money they could save.

Not Considering Vehicle Value

Paying high premiums for an older car may not be financially efficient.

Frequently Asked Questions About Car Insurance Deductibles

Is a $1,000 deductible too high?

Not necessarily. For drivers with stable finances and emergency savings, a $1,000 deductible is often considered reasonable.

Can I change my deductible later?

Yes. Most insurance companies allow policyholders to change deductibles during policy renewal periods.

Do I pay the deductible to the repair shop?

Usually yes. You pay the repair shop your deductible, and the insurance company pays the rest.

Is it better to choose the lowest deductible?

Not always. Lower deductibles increase insurance premiums, which can cost more over time.

Final Thoughts

Car insurance deductibles play a crucial role in determining both your insurance premiums and financial responsibility after an accident. Understanding how deductibles work helps you make smarter decisions about your coverage.

A higher deductible lowers your monthly insurance costs but requires more out-of-pocket payment when filing a claim. A lower deductible offers greater financial protection during accidents but increases your premium.

The best deductible depends on your personal situation, including your savings, driving habits, vehicle value, and risk tolerance.

Before selecting a deductible, take time to compare premium differences and consider how much you could realistically afford if an accident occurs. By choosing wisely, you can strike the right balance between affordable insurance and financial security.