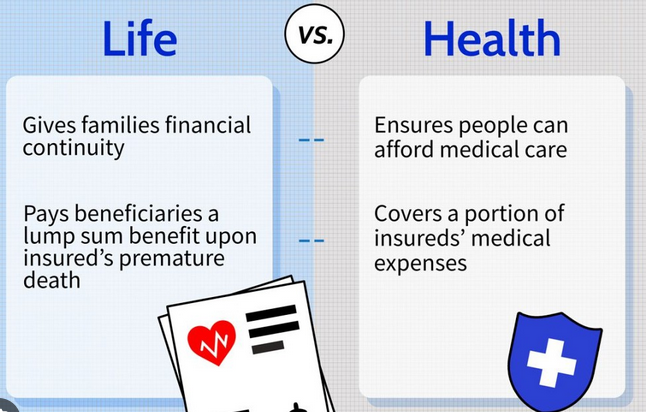

Understanding insurance policies can be confusing, especially when terms like health insurance and medical insurance are often used interchangeably. Many people assume that both mean exactly the same thing, but in reality, there are subtle differences between them. Knowing how these two types of insurance work can help individuals choose the right policy for their needs and protect themselves from high healthcare costs.

Healthcare expenses around the world are rising rapidly. From routine checkups to emergency surgeries, the cost of treatment can put a significant financial burden on individuals and families. Insurance coverage plays a critical role in reducing these expenses and ensuring that people receive proper medical care without worrying about large bills.

In this detailed guide, we will explore the key differences between health insurance and medical insurance, how each works, what they cover, and how to decide which one is the best option for you.

Understanding Health Insurance

Health insurance is a broad type of coverage that protects individuals from various healthcare expenses. It is designed to cover a wide range of medical services including hospitalization, preventive care, diagnostic tests, prescription medications, and sometimes even mental health support.

When someone buys a health insurance policy, they agree to pay a regular premium to the insurance provider. In return, the insurance company pays part or all of the medical expenses depending on the policy terms.

Health insurance is considered comprehensive because it includes both preventive and treatment-based services. This means policyholders can receive coverage for routine health checkups, vaccinations, screenings, and other services that help prevent diseases.

One of the main goals of health insurance is not only to treat illness but also to encourage people to maintain good health through early detection and preventive care.

Understanding Medical Insurance

Medical insurance is often viewed as a narrower type of insurance that focuses primarily on covering medical treatments and hospital expenses. It is usually activated when a person becomes sick or needs medical attention.

Unlike broader health insurance plans, medical insurance mainly pays for expenses such as doctor consultations, hospitalization, surgery, medications, and diagnostic tests related to illness or injury.

Medical insurance is generally designed to reduce the financial burden of unexpected medical emergencies. For example, if someone requires surgery or emergency treatment after an accident, medical insurance helps cover the costs involved.

While medical insurance provides essential protection, it may not always include preventive services or wellness benefits that are commonly included in comprehensive health insurance plans.

Key Differences Between Health Insurance and Medical Insurance

Although both types of insurance aim to reduce healthcare costs, they differ in several ways. Understanding these differences can help individuals choose the right type of coverage.

1. Scope of Coverage

The most significant difference between health insurance and medical insurance is the scope of coverage.

Health insurance usually offers broader coverage. It may include preventive care, mental health support, maternity benefits, wellness programs, and sometimes dental or vision services.

Medical insurance focuses mainly on treatment-related expenses such as hospitalization, doctor visits, surgery, and prescription medications.

Because of its wider scope, health insurance is often considered a more comprehensive protection plan.

2. Preventive Care Coverage

Health insurance plans typically cover preventive services. These services include health screenings, routine checkups, vaccinations, and early disease detection tests.

Preventive care helps identify health problems at an early stage, which can reduce the severity of illnesses and lower long-term medical costs.

Medical insurance, on the other hand, may not always include preventive services. Its main focus is covering treatment costs after a person becomes ill or injured.

3. Wellness and Lifestyle Benefits

Another major difference lies in wellness benefits. Many health insurance plans include wellness programs that promote healthy lifestyles. These programs may include fitness incentives, mental health counseling, nutrition guidance, and stress management support.

Medical insurance typically does not offer these additional benefits. Its primary purpose is to pay for medical treatment rather than encourage long-term health improvement.

4. Cost and Premiums

Because health insurance offers broader coverage, its premiums may sometimes be higher compared to medical insurance plans. However, the higher cost often reflects the larger number of services included in the policy.

Medical insurance may have lower premiums but might require higher out-of-pocket payments for services that are not covered.

Individuals must carefully evaluate the overall value of the coverage rather than simply focusing on the monthly premium.

5. Coverage for Chronic Conditions

Health insurance plans often provide better support for managing chronic conditions such as diabetes, heart disease, or asthma. These plans may include regular monitoring, medications, and specialist consultations.

Medical insurance may cover treatments related to chronic diseases but may not include comprehensive long-term management programs.

6. Preventive vs Reactive Approach

Health insurance takes a preventive approach by encouraging regular health monitoring and early diagnosis.

Medical insurance follows a reactive approach, meaning it mainly helps once a medical issue has already occurred.

This distinction plays a significant role in long-term healthcare management.

Why Health Insurance Is Important

Health insurance is an essential financial tool that protects individuals from unexpected healthcare expenses. Without insurance, even a minor medical emergency can lead to significant financial strain.

One of the biggest advantages of health insurance is access to quality healthcare services. Policyholders can visit doctors, undergo tests, and receive treatments without worrying about paying the entire cost themselves.

Health insurance also promotes preventive care, which helps reduce the risk of serious illnesses in the future.

Additionally, having insurance can provide peace of mind, knowing that financial support is available during medical emergencies.

Benefits of Medical Insurance

Although medical insurance may not offer the same level of coverage as comprehensive health insurance, it still provides valuable protection.

One of the main benefits of medical insurance is affordability. Many medical insurance plans are designed to cover essential treatments at a lower premium.

These plans are especially useful for individuals who want basic coverage for emergencies and hospital treatments.

Medical insurance also helps reduce the cost of surgeries, hospital stays, and medications that can otherwise become very expensive.

For people who already have good health and do not require frequent medical visits, medical insurance may provide sufficient protection.

Types of Health Insurance Plans

Health insurance policies can come in several different forms, depending on the coverage and structure of the plan.

Individual Health Insurance

Individual health insurance covers a single person. It provides financial protection against medical expenses such as hospitalization, doctor visits, and treatments.

This type of plan is suitable for people who want personalized coverage based on their health needs.

Family Health Insurance

Family health insurance covers multiple family members under a single policy. It typically includes spouses, children, and sometimes parents.

This plan is often more cost-effective than purchasing separate policies for each family member.

Employer-Sponsored Health Insurance

Many companies offer health insurance as part of employee benefits. Employer-sponsored plans are often more affordable because the employer may share part of the premium cost.

These plans usually provide comprehensive coverage for employees and sometimes their dependents.

Government-Sponsored Health Insurance

Some countries offer government-funded health insurance programs that provide coverage for citizens, particularly low-income individuals or elderly populations.

These programs aim to ensure that everyone has access to essential healthcare services.

Types of Medical Insurance Plans

Medical insurance also comes in various forms, focusing mainly on treatment-related coverage.

Hospitalization Insurance

Hospitalization insurance covers expenses related to hospital stays, including room charges, surgery costs, and medical procedures.

This type of plan is useful for protecting against large hospital bills.

Surgical Insurance

Surgical insurance specifically covers the costs associated with surgical procedures. It helps reduce the financial burden of operations and related treatments.

Critical Illness Insurance

Critical illness insurance provides a lump-sum payment if the policyholder is diagnosed with a serious disease such as cancer, heart attack, or stroke.

The payout can be used for treatment, recovery, or other financial needs during illness.

Factors to Consider When Choosing Between Health and Medical Insurance

Selecting the right insurance policy requires careful evaluation of several factors.

Personal Health Needs

Individuals with chronic health conditions or frequent medical needs may benefit more from comprehensive health insurance.

Those who mainly want protection against emergencies may find medical insurance sufficient.

Budget and Premium Costs

Budget plays a major role when choosing insurance coverage. Health insurance may require higher premiums, but it often provides more extensive protection.

Medical insurance may be more affordable but could involve higher out-of-pocket expenses in certain situations.

Family Coverage Requirements

People with families may prefer health insurance plans that cover multiple members under a single policy.

Family coverage can help reduce overall healthcare costs for households.

Network of Healthcare Providers

Some insurance plans have networks of approved hospitals and doctors. It is important to check whether preferred healthcare providers are included in the network before purchasing a policy.

Common Misconceptions About Health and Medical Insurance

Many people misunderstand how these insurance types work. Addressing common misconceptions can help individuals make better decisions.

They Are Exactly the Same

One of the most common misconceptions is that health insurance and medical insurance are identical. While they share similarities, health insurance generally provides broader coverage.

Insurance Covers Every Expense

Another misconception is that insurance covers all healthcare costs. In reality, most policies include deductibles, co-payments, and exclusions that policyholders must understand.

Young People Do Not Need Insurance

Some individuals believe that insurance is only necessary for older adults. However, unexpected accidents or illnesses can happen at any age, making insurance important for everyone.

The Role of Preventive Healthcare

Preventive healthcare plays an essential role in modern health insurance systems. By encouraging routine checkups and screenings, insurance providers help detect health issues early.

Early detection can significantly reduce treatment costs and improve health outcomes.

For example, regular screenings for conditions such as high blood pressure, diabetes, and certain cancers can identify problems before they become serious.

Health insurance plans that emphasize preventive care contribute to healthier populations and lower healthcare expenses overall.

The Financial Impact of Medical Emergencies

Medical emergencies can lead to extremely high costs. Hospitalization, surgeries, medications, and rehabilitation services can quickly add up to thousands of dollars.

Without insurance, individuals may struggle to pay these expenses, which can lead to financial stress or debt.

Insurance coverage acts as a financial safety net, allowing people to focus on recovery rather than worrying about medical bills.

Both health insurance and medical insurance play an important role in protecting individuals from unexpected healthcare costs.

How Insurance Companies Determine Premiums

Insurance premiums are calculated based on several factors. These factors help insurers assess the level of risk associated with providing coverage.

Age is one of the most important factors. Older individuals typically have higher premiums because they are more likely to require medical care.

Health history also affects premium costs. People with pre-existing conditions may pay higher premiums depending on the policy.

Lifestyle habits such as smoking, alcohol consumption, and physical activity can also influence insurance rates.

Location, occupation, and the level of coverage selected are additional factors that determine the final premium amount.

The Future of Health Insurance

Healthcare systems around the world are evolving, and insurance providers are adapting to new trends and technologies.

Digital health services, telemedicine, and wearable health devices are becoming increasingly common. These innovations allow individuals to monitor their health more effectively and receive medical advice remotely.

Insurance companies are also developing personalized health plans based on individual health data.

As healthcare technology advances, insurance coverage is expected to become more flexible, accessible, and preventive-focused.

Conclusion

Health insurance and medical insurance both play vital roles in protecting individuals from the high costs of healthcare. While the two terms are often used interchangeably, they differ in scope, coverage, and purpose.

Health insurance typically provides comprehensive coverage that includes preventive care, wellness programs, and treatment for illnesses. Medical insurance focuses more specifically on covering medical treatments and hospital-related expenses.

Choosing between these two options depends on personal health needs, financial situation, and long-term healthcare goals.