Life insurance is one of the most important financial tools available to protect your family and secure their future. Despite its importance, many people delay buying life insurance because they do not fully understand how it works or believe it is complicated. In reality, life insurance is a simple concept designed to provide financial protection to your loved ones if something happens to you.

For beginners, learning about life insurance can seem overwhelming because there are many different policies, terms, and options available. However, once you understand the basic concepts, choosing the right policy becomes much easier. This guide will explain everything you need to know about life insurance, including how it works, the different types of policies, benefits, and how to choose the right plan for your needs.

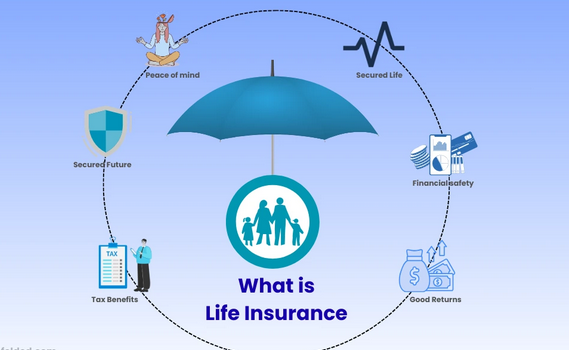

What Is Life Insurance?

Life insurance is a contract between you and an insurance company. In this agreement, you pay regular payments called premiums, and in return the insurance company promises to pay a specific amount of money, known as the death benefit, to your beneficiaries when you pass away.

The purpose of life insurance is to provide financial support to the people who depend on you. This money can help your family cover expenses such as:

-

Daily living costs

-

Mortgage or rent payments

-

Children’s education

-

Medical bills

-

Outstanding debts

-

Funeral expenses

Life insurance ensures that your loved ones remain financially stable even if you are no longer there to support them.

Why Life Insurance Is Important

Many people believe life insurance is only necessary for older individuals, but the truth is that it is important for people of all ages, especially those with financial responsibilities.

Here are some reasons why life insurance is essential.

Financial Protection for Your Family

If you are the primary earner in your household, your income supports your family’s daily needs. Life insurance replaces that income so your family can maintain their lifestyle even after your death.

Paying Off Debts

Many people have debts such as mortgages, personal loans, or credit card balances. Life insurance helps your family pay these debts so they do not become a financial burden.

Covering Funeral Expenses

Funeral and burial costs can be expensive. Life insurance can cover these costs so your family does not have to struggle financially during a difficult time.

Supporting Children’s Future

Life insurance can help ensure your children’s education and future plans are not affected if something happens to you.

Peace of Mind

One of the biggest benefits of life insurance is peace of mind. Knowing your loved ones will be financially protected provides comfort and security.

How Life Insurance Works

Understanding how life insurance works will help you make better financial decisions.

The process typically involves four simple steps.

1. Choosing a Policy

You select a life insurance policy that suits your financial needs and goals. Policies differ based on coverage amount, duration, and cost.

2. Paying Premiums

You pay a premium to the insurance company regularly. Premiums can be paid monthly, quarterly, or annually.

3. Coverage Period

Your policy remains active as long as premiums are paid. During this period, you are covered by the policy.

4. Claim Payment

If the insured person dies during the coverage period, the insurance company pays the death benefit to the chosen beneficiaries.

Types of Life Insurance

There are several types of life insurance policies, but the most common ones are term life insurance and permanent life insurance.

Understanding these options helps beginners choose the right policy.

Term Life Insurance

Term life insurance is the simplest and most affordable type of life insurance.

It provides coverage for a specific period, such as:

-

10 years

-

20 years

-

30 years

If the insured person dies during this term, the beneficiaries receive the death benefit. If the term expires and the policyholder is still alive, the coverage ends.

Advantages of Term Life Insurance

-

Lower premiums

-

Simple and easy to understand

-

Ideal for temporary financial responsibilities

-

High coverage for lower cost

Disadvantages

-

No cash value

-

Coverage ends after the term

-

Premiums may increase when renewing

Term life insurance is often recommended for beginners because it offers affordable protection.

Whole Life Insurance

Whole life insurance is a type of permanent life insurance that provides lifetime coverage.

As long as premiums are paid, the policy remains active for your entire life.

One unique feature of whole life insurance is that it builds cash value over time. This means a portion of your premium is invested, and the value grows gradually.

Benefits of Whole Life Insurance

-

Lifetime coverage

-

Cash value accumulation

-

Fixed premiums

-

Financial stability for beneficiaries

Drawbacks

-

Higher premiums

-

More complex than term insurance

-

Lower investment flexibility

Universal Life Insurance

Universal life insurance is another form of permanent life insurance that offers more flexibility.

It allows policyholders to adjust their premiums and coverage amounts over time depending on their financial situation.

Key Features

-

Flexible premiums

-

Adjustable death benefits

-

Cash value growth

-

Long-term financial planning benefits

However, universal life insurance requires more management and understanding compared to term policies.

Key Life Insurance Terms Beginners Should Know

Before buying a policy, it is important to understand some basic life insurance terms.

Premium

The amount you pay to the insurance company to keep your policy active.

Death Benefit

The amount of money paid to your beneficiaries after your death.

Beneficiary

The person or people who receive the life insurance payout.

Policyholder

The person who owns the life insurance policy.

Cash Value

Savings or investment component in certain permanent life insurance policies.

Underwriting

The process insurance companies use to evaluate your health, lifestyle, and risk before approving a policy.

Who Needs Life Insurance?

Life insurance is beneficial for many different types of people.

Parents

Parents should consider life insurance to ensure their children are financially protected.

Married Couples

Life insurance protects spouses from financial hardship if one partner passes away.

Homeowners

If you have a mortgage, life insurance can help your family pay off the loan.

Business Owners

Life insurance can protect businesses by providing funds to cover debts or replace key employees.

Young Professionals

Buying life insurance at a younger age can help lock in lower premiums.

How Much Life Insurance Do You Need?

Choosing the right coverage amount is one of the most important decisions.

A common guideline is to buy coverage that is 10 to 15 times your annual income.

However, your exact needs depend on several factors.

Income Replacement

Calculate how many years your family would need financial support.

Outstanding Debts

Include mortgages, car loans, and credit card balances.

Education Costs

Consider the future cost of your children’s education.

Living Expenses

Estimate daily household expenses your family would need to cover.

Funeral Costs

Funeral expenses can range from several thousand dollars to much more depending on arrangements.

By considering all these factors, you can determine the appropriate coverage amount.

Factors That Affect Life Insurance Premiums

Life insurance premiums vary depending on several factors.

Age

Younger people usually pay lower premiums because they are considered lower risk.

Health

Your medical history and current health condition affect your premium.

Lifestyle

Smoking, alcohol use, and risky activities can increase premiums.

Occupation

Dangerous jobs may result in higher premiums.

Coverage Amount

Higher coverage amounts lead to higher premiums.

Policy Type

Permanent policies generally cost more than term policies.

The Best Time to Buy Life Insurance

Many people delay buying life insurance, but the best time to buy is as early as possible.

There are several advantages to buying life insurance when you are young.

-

Lower premiums

-

Better health eligibility

-

Longer coverage period

-

Greater financial security

Waiting too long can result in higher costs or difficulty getting approved.

How to Choose the Right Life Insurance Policy

Selecting the right life insurance policy requires careful planning.

Assess Your Financial Needs

Determine how much financial support your family would need if you were not there.

Compare Policy Options

Look at different policy types and compare benefits and costs.

Check the Insurance Company

Choose a reputable insurance company with a strong financial reputation.

Understand the Policy Details

Make sure you fully understand the policy terms before signing.

Consider Your Budget

Select a policy with premiums you can comfortably afford long term.

Common Life Insurance Mistakes Beginners Should Avoid

Many beginners make mistakes when purchasing life insurance.

Waiting Too Long

Delaying life insurance can lead to higher premiums.

Buying Too Little Coverage

Insufficient coverage may not fully protect your family.

Choosing the Cheapest Policy

The cheapest policy may not offer the protection you need.

Not Updating Beneficiaries

Life changes such as marriage or children require beneficiary updates.

Ignoring Policy Terms

Always read and understand policy conditions carefully.

Steps to Buy Life Insurance

Buying life insurance is easier than many people think.

Step 1: Determine Your Needs

Calculate the coverage amount required.

Step 2: Research Policies

Compare different insurance companies and policy types.

Step 3: Get Quotes

Request quotes from multiple insurers to find the best deal.

Step 4: Complete the Application

Fill out an application and provide necessary personal information.

Step 5: Medical Examination

Some policies require a medical exam to assess health.

Step 6: Policy Approval

Once approved, you begin paying premiums and your coverage becomes active.

Can You Have Multiple Life Insurance Policies?

Yes, it is possible to have more than one life insurance policy.

Some people combine different policies to meet their needs. For example:

-

One term policy for income replacement

-

Another policy for mortgage protection

-

A permanent policy for long-term financial planning

However, it is important to ensure the total coverage remains affordable.

What Happens If You Stop Paying Premiums?

If you stop paying premiums, the outcome depends on your policy type.

Term Life Insurance

The policy will lapse, meaning coverage ends.

Permanent Life Insurance

Some policies may use accumulated cash value to keep the policy active temporarily.

If the policy lapses completely, you lose coverage.

Life Insurance and Taxes

In many cases, life insurance benefits are tax-free for beneficiaries.

However, tax rules can vary depending on the country and specific circumstances. Consulting a financial advisor can help clarify tax implications.

Final Thoughts

Life insurance is a powerful financial tool that protects your loved ones and ensures their financial stability in difficult times. While the topic may seem complicated at first, understanding the basics makes it much easier to choose the right policy.

For beginners, the key steps are learning how life insurance works, determining how much coverage you need, and selecting a policy that fits your financial goals and budget. Whether you choose term life insurance for affordability or permanent life insurance for long-term planning, the most important thing is to take action and secure protection for your family.